10 lessons learned on fundraising ops

The first responsibility I had as a startup operator was standing up my company’s sales funnel. The second was managing our seed fundraise. Through running these two processes, I realized sales ops and fundraising ops are eerily similar. While sales ops is about improving efficiency and effectiveness to sell more product and hit revenue targets, fundraising ops is doing so to sell equity and hit fundraising targets.

There’s tons of foundational startup sales resources out there (Founding Sales was my bible), but the same just doesn’t exist for fundraising. Fundraising ops seems to be lore, passed down across startup whisper networks.

So, I’m sharing with you my lessons learned on how to engineer a competitive fundraise process with investors. This post is for first-time, underdog and underrepresented founders raising a pre-seed or seed, and who may have odds stacked against them without a built-in investor network, vocabulary and resources. (Women-founded startups raised just 2% of VC funding, and Black founders received only 0.5% last year.) I also hope that experienced founders can take something away.

The ten lessons:

- Qualify the investors that you want for your startup.

- Build investor relationships ahead of your raise.

- Hunt down the warmest intro within your network.

- Treat fundraising like a full-time and timeboxed job.

- Channel the investor mindset in overpreparing for your pitch.

- Evangelize your gems in every meeting — and protect your risks.

- Optimize for maximum face time by dripping just enough materials to get you that next meeting.

- Create a surround sound effect to keep your startup top of mind.

- Keep calm, remember to diligence and negotiate thoroughly.

- Be kind.

1. Qualify the investors that you want for your startup.

Investors will always want to grab coffee with you, because seeing deals is career currency and it’s their job not to miss you. However, it’s your job to be laser-focused on spending time with the right investors for your business to close one round.

I think back to this piece of wisdom from Sarah Tavel, “You owe it to yourself not just to look at the list of people who reached out, but to ask yourself, “who do I want?”, and then find a way to them.”

Questions to figure out if an investor is one that you want on your cap table:

Is the firm a fit for your business?

- What’s their fund size?

- Thesis?

- Stage of investment?

- Preferred position to lead, co-lead, or follow?

- High-signal portcos or competitors in their portfolio that would conflict them out?

Is the investor a fit?

- What industries or focus areas do they invest in?

- Do they understand your business and vision?

- Once you get connected, is the investor helpful to you?

The best way to keep track of the above is through your investor CRM, your rolodex to build and track relationships and targets. You can compile a starting list via Pitchbook pulls, Linkedin searches, asking nodes in your network (see #2), perusing industry newsletters or Slack channels for active firms.

Here’s an investor CRM template based on the one I used for my last startup’s seed round. You can use Airtable or Google Sheets which are both free and collaborative database tools.

2. Build investor relationships ahead of your raise.

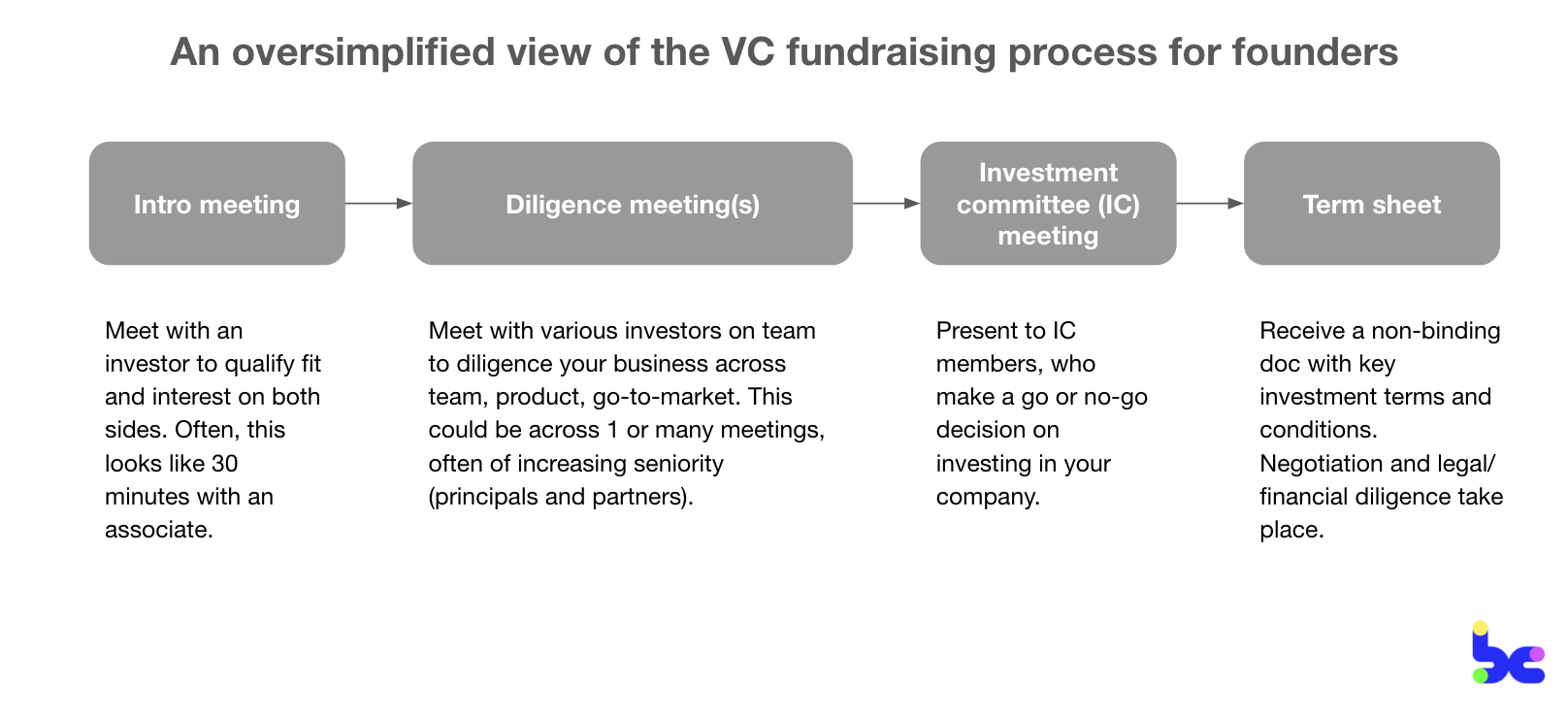

I used to think that the fundraising process — from first meeting to securing the term sheet — looked like this:

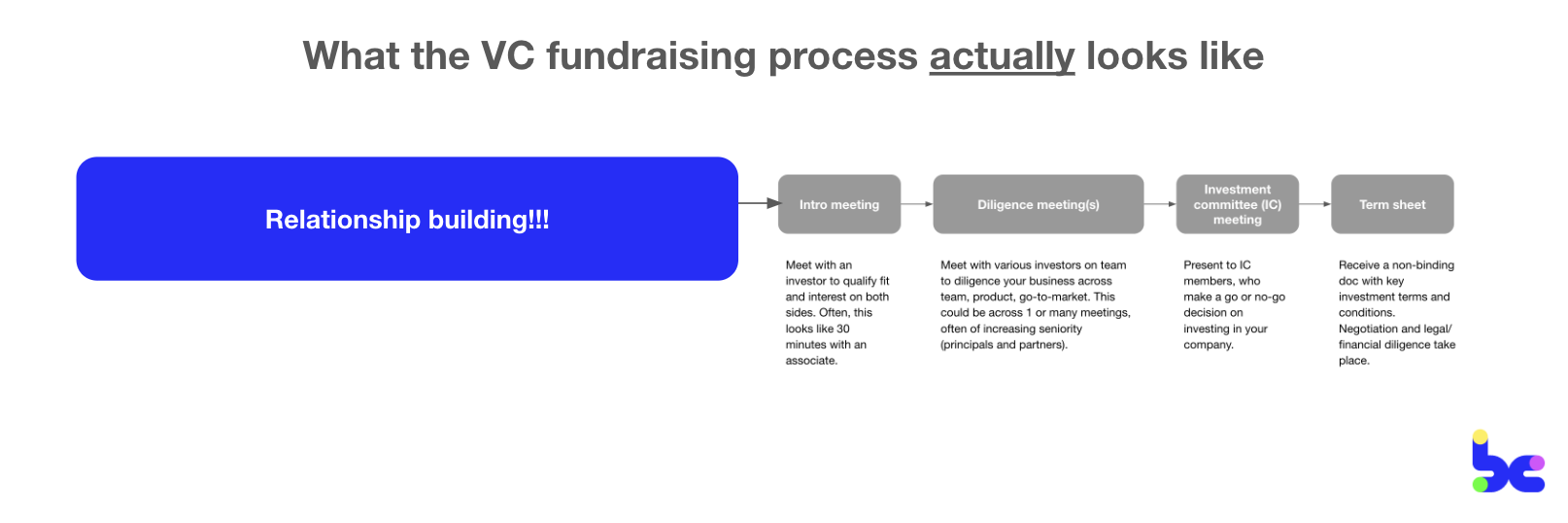

In reality, it looks more like this:

Investor relations is an all-year round responsibility. For investors, they’re diligencing you as the right founder for the business and prefer getting to know you over an extended period of time. For founders, you similarly benefit from the longer “dating” period; plus, it’s much easier to line up meetings when you do kick off a raise with relationships already built in.

The trick is to remember that you control your calendar. While this may seem obvious, I’ve noticed this power dynamic where founders have a hard time saying “no” to investors. That’s when investor relations can quickly snowball into a distraction. Instead, you can timebox coffees with investors so you don’t incur switching costs (for example, Thursday mornings), and know that it’s okay to push meetings back if your week turns chaotic.

The best founders leverage investor meetings as added fuel towards product-market fit. An investor’s job is understanding market trends to predict the future and building up the industry networks to help them source, diligence, win and support their startups. You can go into meetings with specific asks for them: customer intros, a case study on how one of their similar portcos navigated pricing, or brainstorming through a GTM challenge you’re facing.

You want to jump into fundraising from a place of strength: with existing investor relationships, a target list of investors, and warm intros ID’d to those who you haven’t met yet.

3. Hunt down the warmest intro within your network.

Not all warm intros are made equal. There’s a spectrum of “warm”-ness: On one end, is someone who intro’s you to an investor after having met them once in a 30-min Donut. That’s lukewarm at best. On the other extreme, is a founder in an investor’s existing portfolio who has worked directly with you and can speak in detail to your background and outputs. That’s the intro you’re looking for — a warm intro who has a trusted relationship to both you and the investor.

Three strategies you can run in identifying the warmest, high-quality intro in:

-

Share an external version of your CRM with superconnectors in your network, and ask them to “sign up” in a dedicated column for potential intros they can make. These superconnectors are friendly nodes in your network that have tons of relationships with investors. Often times, they’re seen as community builders or organizers. (For those building in healthtech, here’s a list of healthtech communities.)

-

Go on an investor’s Linkedin profile and reach out to mutual connections to see if they’d be open to making an intro. You can try a few mutuals, to identify the strongest connection.

-

If all warm routes are exhausted, reach out cold and thoughtfully. You’d be surprised at how effective a thoughtful cold email can be, especially if it’s framed as mutually beneficial and value-add to the investor. Not just, “Hey, I want to pick your brain.”

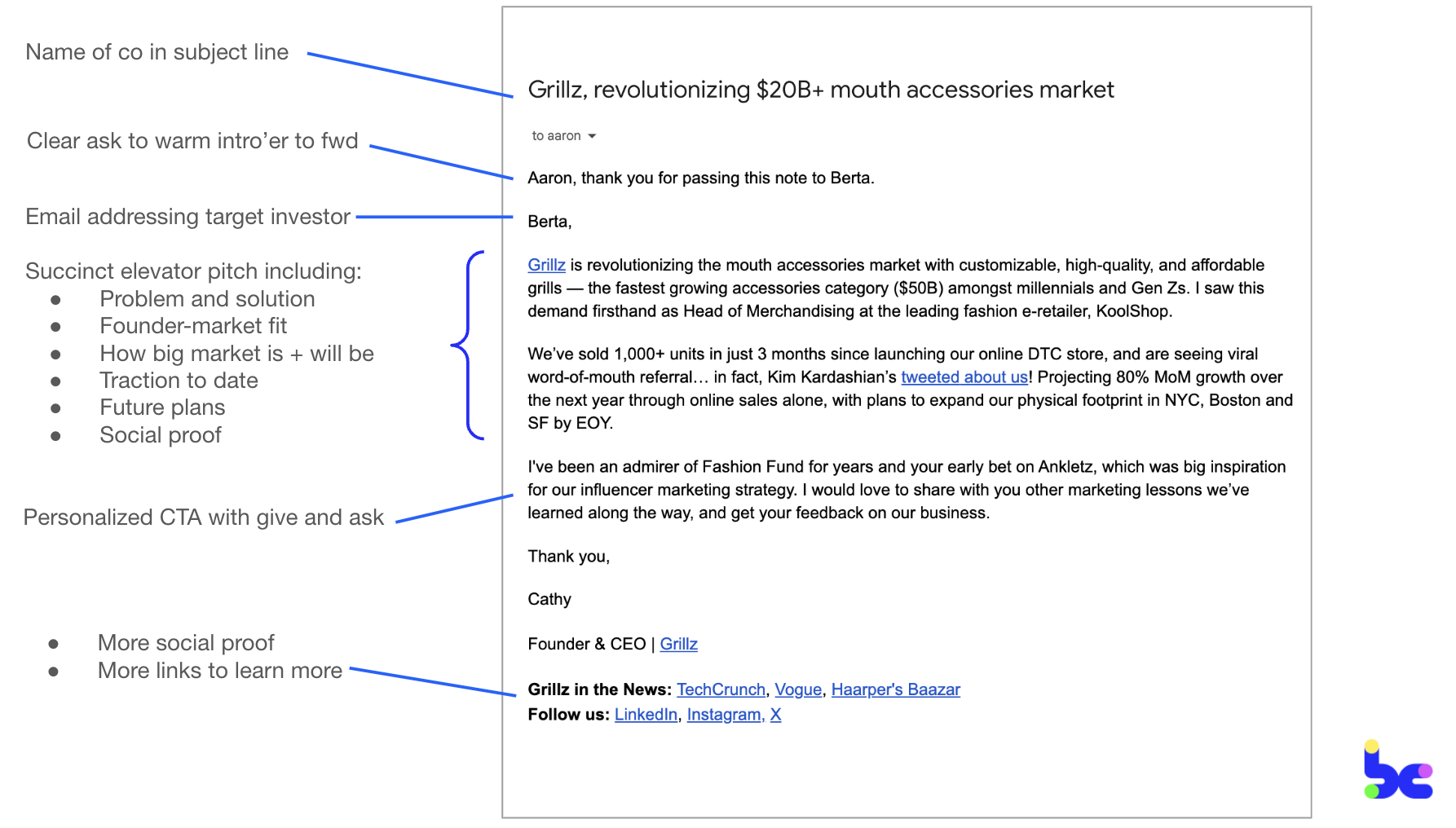

And lastly, make intros so easy of an ask with forwardable and personalized emails, that people can’t say no. Here’s an example of a forwardable to make the double opt-in warm intro for a fictional startup (although if anyone wants to start a grills co, hit me up). These ingredients can also be applied to cold intros:

4. Treat fundraising like a full-time and timeboxed job.

It’s better to take ten quality intros a day to secure that term sheet from a lead in a month, than to spend half a year taking a few meetings a day with investors who may not be fits.

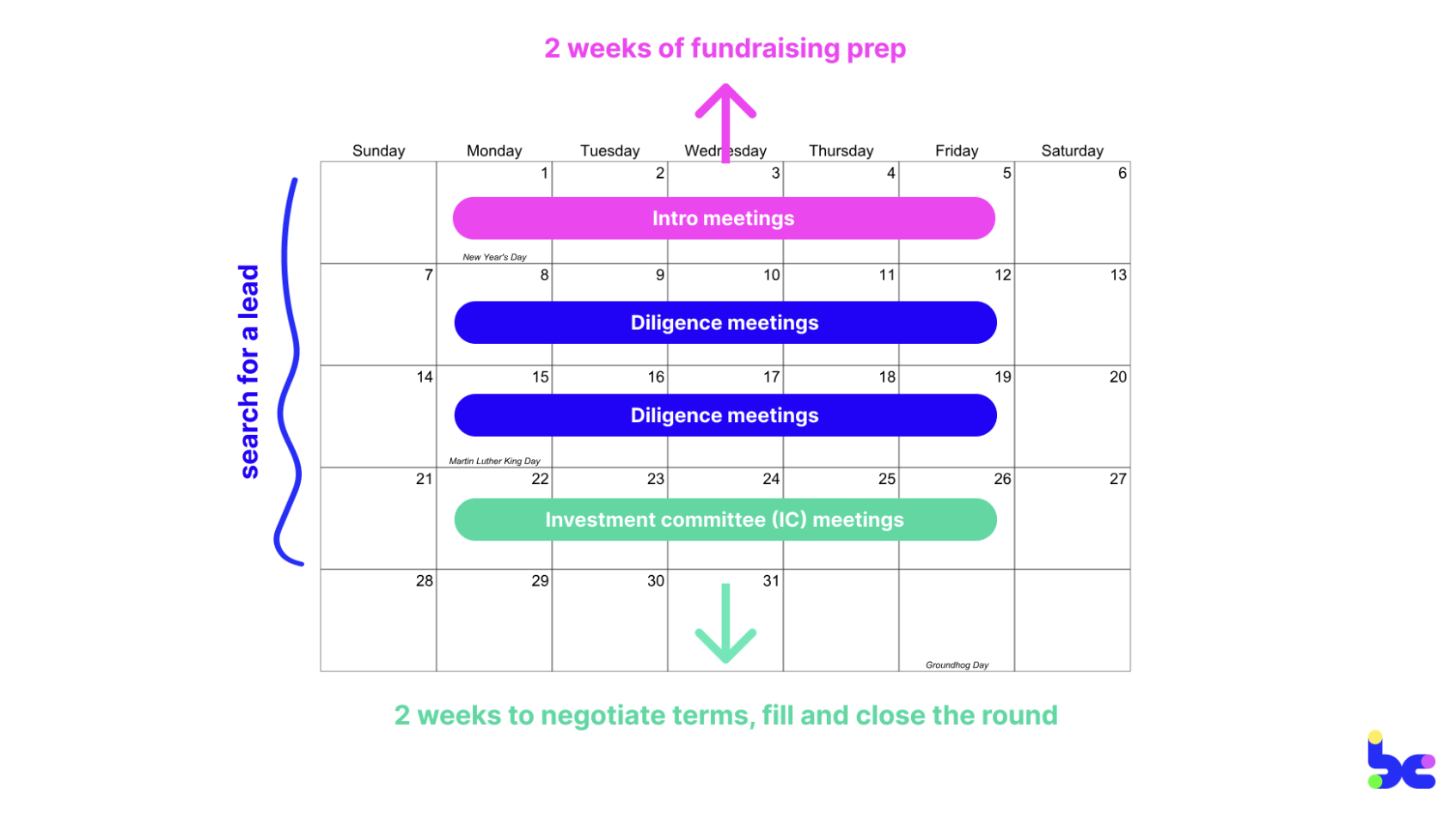

Here’s what a timeboxed seed fundraise could look like, in securing a lead investor:

🔧Tooltip:

The lead investor is often the first investor you’re searching for to commit to your round, because they contribute a meaningful percentage of the round (sometimes, 50%~) and are responsible for negotiating and setting the terms with you and other follow-on investors.

This cadence puts pressure on investors to move fast and through funnel at similar times. You’re generating a sense of competition, which ideally ends with having multiple term sheets that you can choose between or leverage to negotiate better terms.

Let’s dig into what this might mean:

- Work backwards from your target kickoff date. You’re fast approaching the milestones to unlock your seed raise and have a target kickoff date on the calendar. Spend the two weeks prior prepping: lining up intro meetings to investors; crafting your pitch, data room and materials; scheduling a few practice pitches with friendlies.

🔧 Tooltip:

Holidays can destroy momentum. You probably don’t want to kick off a fundraise in August or December, because you’ll be met with a myriad of OOO’s through Labor Day and the winter holidays. It can also be quiet in mid-March, where Partners may be out for Spring Break with their families.

-

Use the intro meeting as a qualifier. You want to line up as many 30-min intro meetings as possible, optimizing for breadth. Treat those intros as qualifying conversations, and be laser focused on winnowing that funnel down to qualified leads (aka the investors you want), putting others like potential follow-on investors on hold.

-

Create batches of investors. One founder gave me the tip that they batched investors into waves, where they scheduled wave 1 in 2 to 3 days, had a break in between, and then had wave 2, and so on. This allowed them to get a term sheet in the first batch, which created momentum for the next. This cadence also gives you time to iterate and fix your story and deck.

-

Iterate your pitch regularly. While you can’t get fixated on rejections (or else you’ll spiral into a puddle of self-doubt), reasons of why an investor passed can be good to reflect on from time-to-time to see if you can iterate and improve your pitch. I had a column in our investor CRM where I’d write down reasons an investor passed, revisit at the end of week, and determine what feedback was worth incorporating into our story and pitch.

-

Align on expectations and next steps at the end of meetings. At the end of meetings, help investors match your tempo by being explicit about your timeline, “We remain very excited about XFirm, but as you know, we’re running a competitive process and will likely close this round in X weeks’ time.” You can also get a pulse check by asking, “How are you feeling about us?” If good, then ask for next steps in making a decision. If not so good, then you at least get a straightforward answer and know to chase other leads.

Given your priority for the next two months will be fundraising, make sure to prep the rest of your team, especially if they’ve never been through the fundraising context before. This means getting other team members to cover for your usual workstreams; and prepping leadership to jump in during diligence. For example, your CTO might be pulled in to do a product demo, and beyond just the demo, they should be able to pitch your business.

5. Channel the investor mindset in overpreparing your pitch.

The best early-stage fundraisers are magical storytellers. You’re crafting narratives that paint a vision of the future that get investors clambering to be on the journey. 99% of magical storytellers get to that point with deep preparation and practice. So overprepare.

Yes, it may sound alarmist. But three reasons I emphasize overpreparing:

- You should have a plan and hypotheses of how you’re going to be the next unicorn, that you can succinctly and intelligently articulate. And that takes a lot of work and time to get to.

- You want to combat nerves that may be on overdrive. Fundraising is a high pressure environment where you’ll have to adapt quickly on the fly. Some investors will sit patiently through a 5-min pitch, while others will pepper you with questions from the start.

- And lastly, investors are sometimes asking questions not to diligence your business, but to diligence you. They want to know that you’re smart. So you should sound smart.

As you overprepare, channel the investor’s mindset. While the founder’s day-to-day may be in the weeds — focused on bug fixes for a product launch or setting next quarter’s sales targets — you need to switch into the longer-term narrative — of your product strategy for the next few years and how that’ll unlock $XXM revenue and your next fundraise. At the end of the day, what an investor cares about is if your business will generate big returns for their Limited Partners over a 7-10 year time horizon through a liquidity event.

Investors have diligence checklists that they use to evaluate companies. While checklists vary, prepping your pitch to answer the ten most common questions will get you 80% of the way there. Sequoia’s How to Write a Business Plan outlines a pitch skeleton and common questions.

There’s also a bunch of less obvious, trickier questions:

- Q: What valuation are you looking for? A: Don’t give a valuation.

- Q: Are your existing investors participating in this round? A: Of course they’re interested in participating, and can meet new investors’ ownership targets too.

- Q: How much are you raising? A: Give one number (not a range!) based on value-creating milestones.

- Q: Who are potential acquirers for your company? A: Explain that while you can see many potential buyers (naming a few categories and why they’d be interested), that you’re building this company with a clear path to IPO.

A good way to test that your pitch is investor ready ahead of fundraising is by practicing with a few friendlies in your network who’ve lived the investor mindset, but aren’t one of your targets this round. For example, ex-investors turned startup builders who’ve sat on both sides of the table.

6. Evangelize your gems in every meeting — and protect your risks.

While you should have a five-min pitch ready that complements your deck, you should also have a 30-sec pitch prepared, that can be repeated like mantra in every meeting, rooftop happy hour, and of course, elevator.

Your elevator pitch should include three to four bullets, that give investors a clear understanding of your business (the problem, solution, market), and the key “gems.”

Your two to three gems are what you want to shout from the rooftops and elevate — whether that’s your unique differentiator that’ll blow away all the competitors, or impressive growth numbers over the past months. Similarly, knowing the holes in your armor where you may not have the strongest answers allows you to craft a story that avoids bringing up or plays down these risks.

Make sure to repeat your elevator pitch in every meeting, even if it’s the second or third meeting with an investor, and definitely if there are new investors in the room. Investors can see ten+ pitches every day and may want a refresher, or may not have briefed new investors on previous conversations.

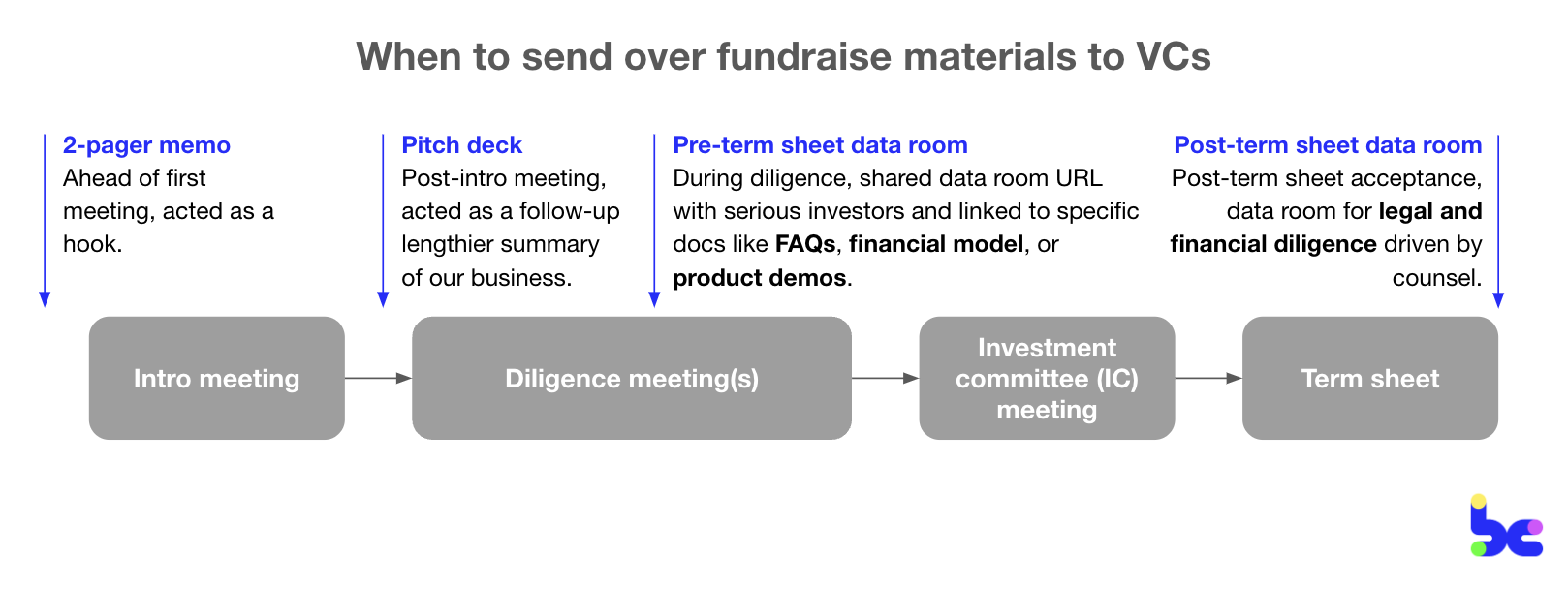

7. Optimize for maximum face time by dripping just the right amount of materials to get you that next meeting.

Good investment materials should do three things:

- Be that hook to get your foot into meetings.

- Be a source of reference for you and investors: for you as a supporting visual as you pitch, and for investors to easily go back to their team in championing you (which includes writing their investment memo).

- Streamline the fundraising process so you don’t have to repeat the same answers over and over.

There’s a tricky dance of how much info and materials to send over. Counterintuitively, you don’t want to lay out all your cards. If you share your entire data room in the first meeting, investors may take weeks getting back to you because they’re digging through the minutia of details with a fine-tooth comb to find reasons to say “no.” And once they decide to pass, there’s no way to convince them otherwise.

Instead, you want to drip the right amount of materials to get investors excited to take the next meeting. You’re optimizing for as much face time as possible to sell them on you and your vision, and to dissuade them of their concerns. These were the materials and cadence that worked for us:

The 2-pager memo is your no-fluff, all-text summary to reel investors in and as pre-read for deeper conversations during the intro meeting. You can link to it in any warm or cold intro email. We found this better to send over than a deck as it’s easier for an investor to scan through and gives you an opportunity during the intro meeting to create an “ah ha!” moment with the deck narrative; plus, you have an automatic follow-up of sending over the deck post-meeting to keep the conversation going.

The pitch deck serves as the magnum opus of your business, that can be standalone or complement your verbal pitch, and should cover answers to investors’ most common questions.

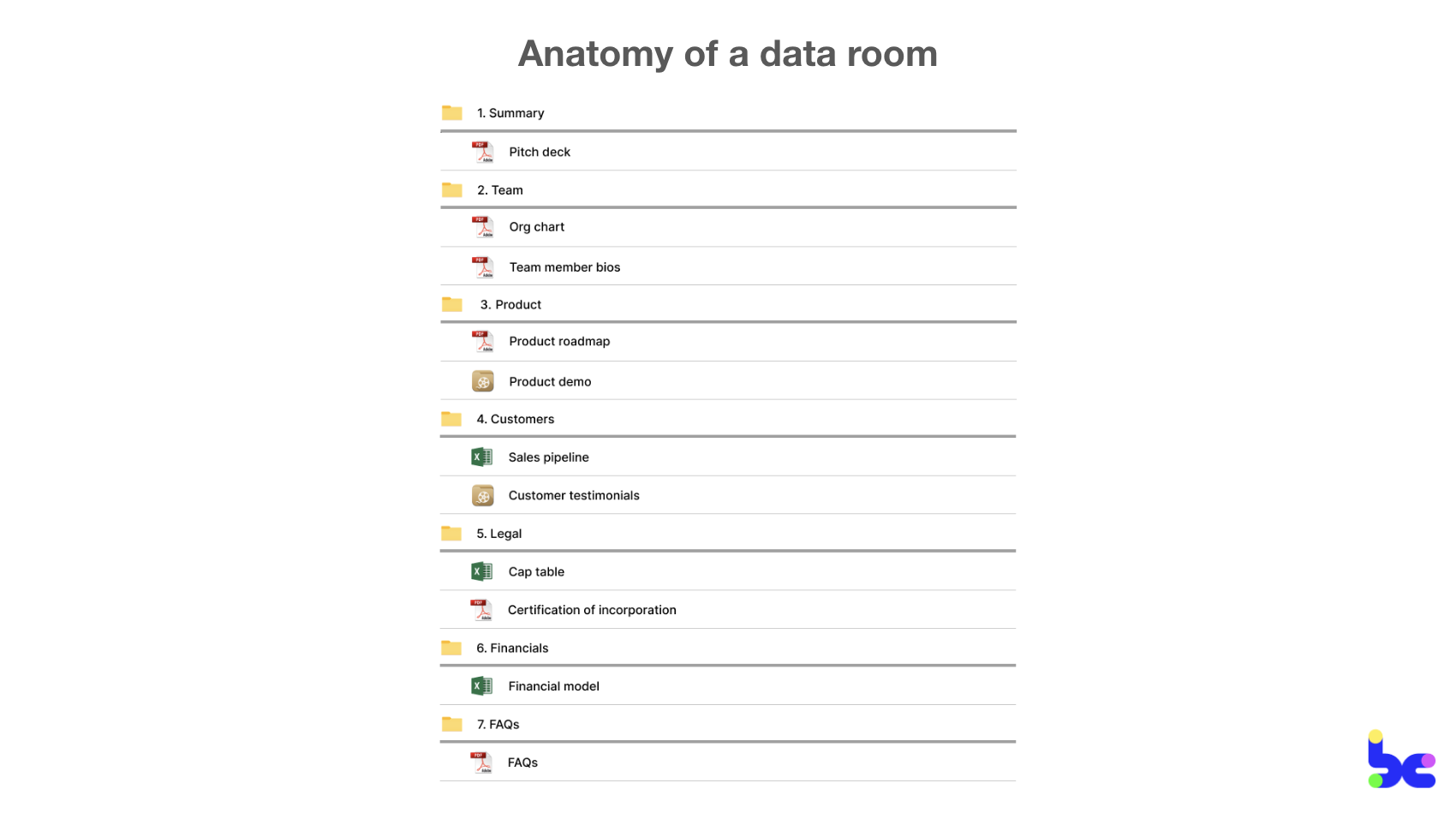

Both of these live in your data room, a folder where all the materials for diligence are housed that you send to qualified investors who are serious about you and farther along in process. What you include in your data room can vary based on your narrative (those gems and risks). For example, if you’re a care delivery provider pioneering a new care paradigm, you may want to include patient metrics or research papers that highlight the outcomes of your model.

Here are docs we had in our data room for our seed:

Two other data room tips:

- If you get asked a question two+ times, write it down in an FAQs doc. This doc answers questions that investors may ask you in follow-ups and that aren’t covered in pitch decks. For example, how you calculated TAM. This is a working doc you can continuously add to and which you can easily pull from or link, so you don’t find yourself retyping the same answers in email.

- Record customer testimonials and product demos to protect customers’ valuable time, your own from making a myriad of intro’s, and the invesetor’s in referencing your customers at short notice. You should still prep your team members and customers to jump on calls with investors.

8. Create a surround sound effect to keep your startup top of mind.

You want investors to have you top of mind as you fundraise. It’s about creating hype and getting them to hear how awesome your business is from multiple sources and angles at the same time.

A few tactics you can use to create that surround sound effect:

- Share investor updates to show continued progress. Tell the story of increased traction during fundraising. You can opportunistically email all investors in process when you hit a startup milestone like closing a new customer logo or exceeding expectations on your sales target for the month. We got a handful of investors in funnel who picked up momentum through these update emails.

- Founder brand building = company brand building. Every founder should be the most enthusiastic sales person and evangelist for their startup. In the early stage, investors index heavily on the founder’s perceived “fit” for the product and market, which makes credible founder PR even more appealing to investors. You can publish thought leadership or announcing company milestones on Linkedin and Twitter.

- Use your warm connects as backchannels. With investors who you’re deep in process with, you can ask warm mutuals (for example, the connect who intro’d you) to send a note vouching for you. Sometimes, investors will backchannel you with mutuals without asking.

9. Keep calm, remember to negotiate and diligence thoroughly.

You’ve got the term sheet in hand. But it’s too early to celebrate. Continue to be in sell mode with your investors, as nothing is done until the money is in your bank account and the round is closed. The investor you bring on board can be on the journey with you for the next seven to ten years.

Firstly, keep calm! While you don’t want to take too much time post-term sheet as that may signal your disinterest to the investor, you should never feel pressured to sign a term sheet right away. Exploding term sheets are a horrible practice. Do be respectful in keeping investors up to date.

🔧 Tooltip:

A good lawyer is always worth it. Do not skimp on legal fees, and make sure they’re locked in before the raise. Founders who switch lawyers during negotiations can slow the process of getting money into the bank significantly.

Secondly, diligence your investors in parallel to negotiating. You can keep your committed investor warm by sharing how excited you are to work with them and asking for a few founder references to learn about how they partner with founders. This allows you do your own diligence while giving you time to go to other investors in funnel and seeing what other offers may come up.

Lastly, I’ve seen founders who become frantic over thinking that they’ll lose out on an offer if they negotiate. The investor has just as much to gain — if not more — by negotiating with you. A term sheet means that they have conviction and they don’t want to lose out either. Make sure you know what terms you’re optimizing for. Is it valuation? Avoiding dilution? (Keep in mind most lead firms are targeting 10-20% ownership.) A strategic partner who can open enterprise doors? This’ll help you prioritize what to negotiate.

10. Be kind.

Speedy communication can contribute to momentum and signal your interest to an investor. So be kind and responsive to all investors.

This includes Associates. There’s this whole Twitter discourse on avoiding Associates. But it’s their job to source and diligence, and they can be powerful champions. An Associate at a firm who led our seed was the one who shepherded us through from cold emailing to helping prep us for IC and term sheet negotiation. And if nothing, be kind to Associates because they can kill deals.

Even if an investor isn’t the right fit or ends up passing on your round, the world is small. They may potentially invest in future rounds or intro you to the right investors and customers.

Closing thoughts

This Tweet by @stuartblitz was one of the inspos behind this post:

If you're in health tech, there are generally only 3 ways to raise new VC money right now:

— Stuart Blitz (@StuartBlitz) January 3, 2024

1) Genuinely don't need it

2) FOMO with an actually competitive process

3) Good fortune

While cloaked in jest, it’s a painful fundraising environment right now for founders. Sharing these lessons is my attempt to level the fundraising field for who can be a venture-backed founder. If you have any other lessons to add, shoot me a message.

A big thank you to Sam Gerstenzang and Claire Pan for their inputs. Fun fact: I met them both via cold emails (can confirm, they do work).